Diligent restaurant inventory management and food cost control are at the heart of profitability for all foodservice operations. A cost control methodology called “Actual vs. Theoretical Food Cost Variance” (AvT) is a powerful way to keep your restaurant’s food costs in check. And the extra profits generated by monitoring those food costs can be astronomical if your operation is taking advantage of the data that’s available. But as often is the case, tracking food costs is exceedingly difficult without access to the right tools and information. In order to control volatile costs, many multi-unit restaurant chains spend tons of time and energy evaluating their spending, holding, and handling of foods to help drive profit (sometimes saving millions in the process). Thankfully, using aninventory management system built for restaurantscan streamline the process and take the guesswork out of calculating AvT. More on that later, but first let’s look at Betty’s Burgers to get a better idea of how tracking food costs through Actual vs. Theoretical Cost Variance works:

Betty's Burgers - Austin vs. Houston:

The video above explores what the actual vs. theoretical food cost variance is, and how it impacts profitability for restaurants.

Let’s look at two locations of a fast-casual restaurant chain called Betty's Burgers:

Betty's Austin Food Costs = 32.1% of Sales

Betty's Houston Food Costs = 32.8% of Sales

To understand how the managers at Betty’s in Austin and Betty’s in Houston manage food costs, we need to considerthe local costs for all ingredients in each restaurant and the menu mix for each restaurant.

What is Food Cost Variance?

It’s important to understand what food cost variance is before we dive deeper into our Betty’s Burgers example.

Theoreticalfood costis what a restaurant’s food costs should be, based on current inventory costs of all ingredients for the meals sold, and assuming perfect portions, no breakage, and no shrinkage.Let's consider the model of a company like Hello Fresh, which offers meal delivery service. In this context, the theoretical food cost would encompass the inventory costs of all ingredients required for their meal kits.

Once you know your restaurant’s theoretical food cost for each menu item, you can compare it to its actual food cost. Actual food cost is the actual cost of all the food that your restaurant used during a given sales period.

The mark of truly great food cost control is how closely a restaurant’s actual costs approaches its theoretical costs. An exact match would mean perfect portioning and no breakage or shrinkage. The difference between the two is the true measure of efficiency in food cost control; it’s called the actual vs. theoretical food cost variance and reducing it to its lowest possible point is the goal in optimizing your restaurant’s food costs.

What is Betty’s Burgers Actual vs Theoretical Food Cost Variance?

By looking at the food cost variance between Betty’s Burgers in Austin and Betty’s Burgers in Houston we can determine which restaurant operator is doing a better job of optimizing their food costs.

AUSTIN LOCATION: FOOD COSTS = 32.1% OF SALES

ACTUAL FOOD COST = 32.1 % OF SALES

THEORETICAL FOOD COST = 29.5% OF SALES

This means Austin's Food Cost Variance is 2.6% of sales.

HOUSTON LOCATION: FOOD COSTS = 32.8% OF SALES

ACTUAL FOOD COST = 32.8 % OF SALES

THEORETICAL FOOD COST = 31.9% OF SALES

This means Houston's Food Cost Variance is only .9% of sales.

Betty's in Houston is doing a far better job managing its food costs, as breakage, shrinkage, and portioning mistakes amount to only 0.9% of sales, while the Austin location is at 2.6% of sales.

What does this mean for Betty’s Burgers?If each restaurant has $1,000,000 in sales per year, then Austin's extra 1.7% of costs contributes to $17,000 in lost profits! If Betty’s Burgers has 24 restaurants and half of them have a similar food cost variance, that’s$204,000 in lost profits per year.

FixYour Food Cost Variance by Fixing Your Profit Leaks

The surest way to drive profit dollars to the bottom line is to identify the biggest “profit leaks” in an operation. You must find where they’re occurring and thendetermine their root causes. Only then will you be able to fix these profit leaks.

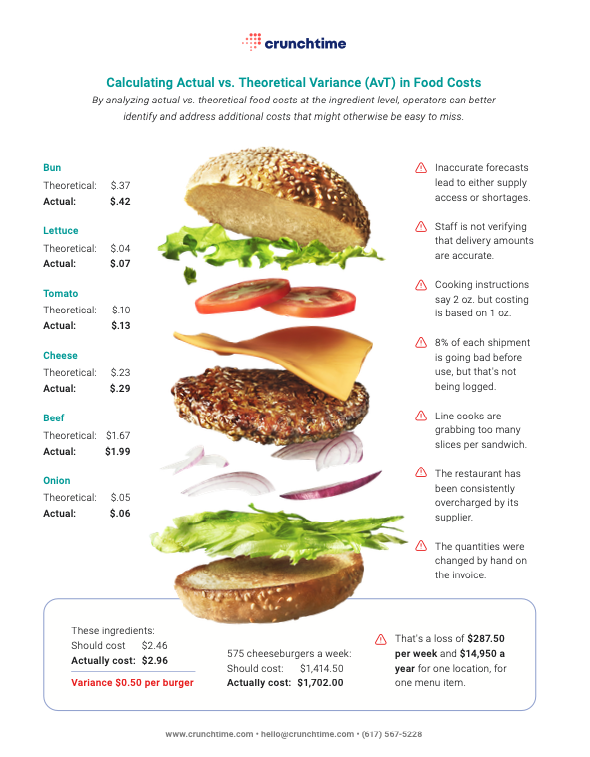

To begin, once the overall variance from theoretical cost is known, the best practice for reducing it requires identifying the individual ingredients with the largest variances by dollar volume, and analyzing their use to spot waste, theft, or overcharges. In a typical operation with hundreds of items in inventory, it can be a daunting task.

The investigation begins with the store that has the highest variance for each spotlighted item. For example, if chicken breasts represent the greatest dollar variance from ideal theoretical cost company-wide, and a restaurant in Albany, NY shows the greatest dollar variance of all stores, the investigation would start in Albany and center on these commonprofit leak areas:

Common Profit Leak Areas:

Receiving. Make sure inventory amounts are accurate.

Invoicing.Make sure costs are correct.

Recipe preparation. Ensure proper usage in preparing recipes to eliminate mistakes.

Portioning.Follow recipe cards to the letter.

Waste tracking.Properly trackwasted food through spoilage.

Other reasons for inventory adjustments like suspicious anomalies could mean there is a theft issue.

What Tools Are Required to Determine Actual vs Theoretical Food Cost?

The accurate measurement of Actual and Theoretical food costs requires the following for every store and commissary in your company:

Accurate local market pricing for all ingredients.

Accurate beginning and ending inventory count to determine usage.

Accurate ingredient amounts specified for all recipes.

A system for accurately recording waste

A system for capturing, in real-time, recipes sold and their associated ingredients’ costs (and for depleting from inventory the individual ingredients)

Having this information on demand enables you totroubleshoot food cost issues in real time. Of course, the best way of processing an overwhelming amount of data, like that of a typical restaurant operation, is with an integratedrestaurant inventory management systemthat does real-time analysis for you - automaticallyacross all your locations.

These days, it seems that food prices are always on the rise. Do you want to learn more about how we can potentially save your restaurant chain millions of dollars in lost profits each year by helping control your food costs? Reach out to us here.